No Country for Old Portals

The payments world moved on. Your portal didn't.

Most collections portals lose 6 out of 10 consumers before they even see their balance. Here's what that's costing you — and what the fix looks like.

There was a world where your portal made sense.

Consumers expected to dig out account numbers from paper letters. Paying anything online felt modern. A clunky login screen was just how the internet worked, and a portal — any portal — put your firm ahead of the pack.

That world is gone. The consumer you're trying to collect from today splits a dinner bill in three taps. Pays for groceries with their phone. Renews insurance in under five minutes without speaking to a human. Payments in their life are instant, mobile, and frictionless — not because they're tech-savvy, but because that's simply how everything works now. Seamless isn't impressive anymore. It's the baseline.

The country changed. And in this new one, there is no place for old portals.

Yours might be one of them. The tell is a sentence you've probably said yourself:

"We have a portal. Consumers can pay online anytime."

You're not wrong. You do have a portal. Consumers can, technically, pay online anytime.

But here's the question nobody in your firm has actually answered: what happens after they click the link?

Not in theory. In reality. With real consumers, on real phones, at 9 pm on a Tuesday.

Because if you haven't looked at that, there's a good chance your portal isn't a self-serve payment channel. It's an expensive dead end — and you're paying to send people to it every single day.

You're paying thousands a month before a consumer even sees your portal

Let's start where most law firm leaders don't: the spend.

Before a single dollar comes in through your portal, you've already paid for:

- Every text message sent with a portal link — per message, per send

- Every email in your outreach cadence

- The portal itself — licensing, implementation, hosting, maintenance

- The staff time spent managing all of the above

Across a meaningful portfolio, that adds up to thousands of dollars a month — all spent to drive consumers to one destination.

Which raises the obvious question: when a consumer actually arrives at that destination, what do they find?

9 pm on a Tuesday: the part of the journey you've never watched

Picture the consumer your text just reached. They have a quiet moment, the kids are asleep, and they've decided tonight's the night they deal with this. They click your link.

Here's what they find:

- A request for an account number from a letter they received two months ago

- A page that doesn't render properly on mobile

- No help text, no guidance, no obvious next step

- An error message when they try their SSN in the wrong field

They don't push through. They close the tab.

They didn't ghost you. Your portal ghosted them.

And there's a quieter cost here too. Consumers have been trained — by their banks, by the news — to be cautious about where they enter payment details. A portal that looks and feels a decade old doesn't just frustrate them. It makes some of them hesitate on a more basic question: is this even legitimate?

That hesitation costs you payments from consumers who were ready to pay. The question is how many. And there's a number that answers it.

6 out of 10 consumers leave before seeing their balance. Do you know your number?

There's a single metric that reveals whether your portal is doing its job:

Verification completion rate — the percentage of consumers who land on your portal and successfully make it past the front door to see their account.

Not traffic. Not clicks. Not sessions. The percentage who actually get in.

Here's the benchmark to know:

- The industry average for a standard collections portal sits below 40%

- That means 6 out of every 10 consumers who clicked your link — with intent to pay — left before they ever saw their balance

- You paid for the message that brought them there. Your portal turned them away.

What's your number? If you don't know, that's the first question to ask whoever manages your portal.

And if your number is anywhere near that average, it's almost certainly because of one — or all — of three design decisions nobody remembers making.

Three design failures bleeding you out right now

These aren't edge cases. They're the default state of most collections law firm portals — and each one is fixable.

1. No pre-fill. Your portal asks consumers to remember an account number from a paper letter sent months ago. Most can't. Most leave.

2. No guided offer. Your portal shows a balance, but it stops there. "Here's what you owe" is not a conversion strategy. A consumer who can't pay in full sees no path forward — so they take no path at all.

3. Wrong channel, wrong delivery. A portal link buried in a letter or a generic email has a fraction of the pull of a text with a pre-filled, one-click link sent at the right time.

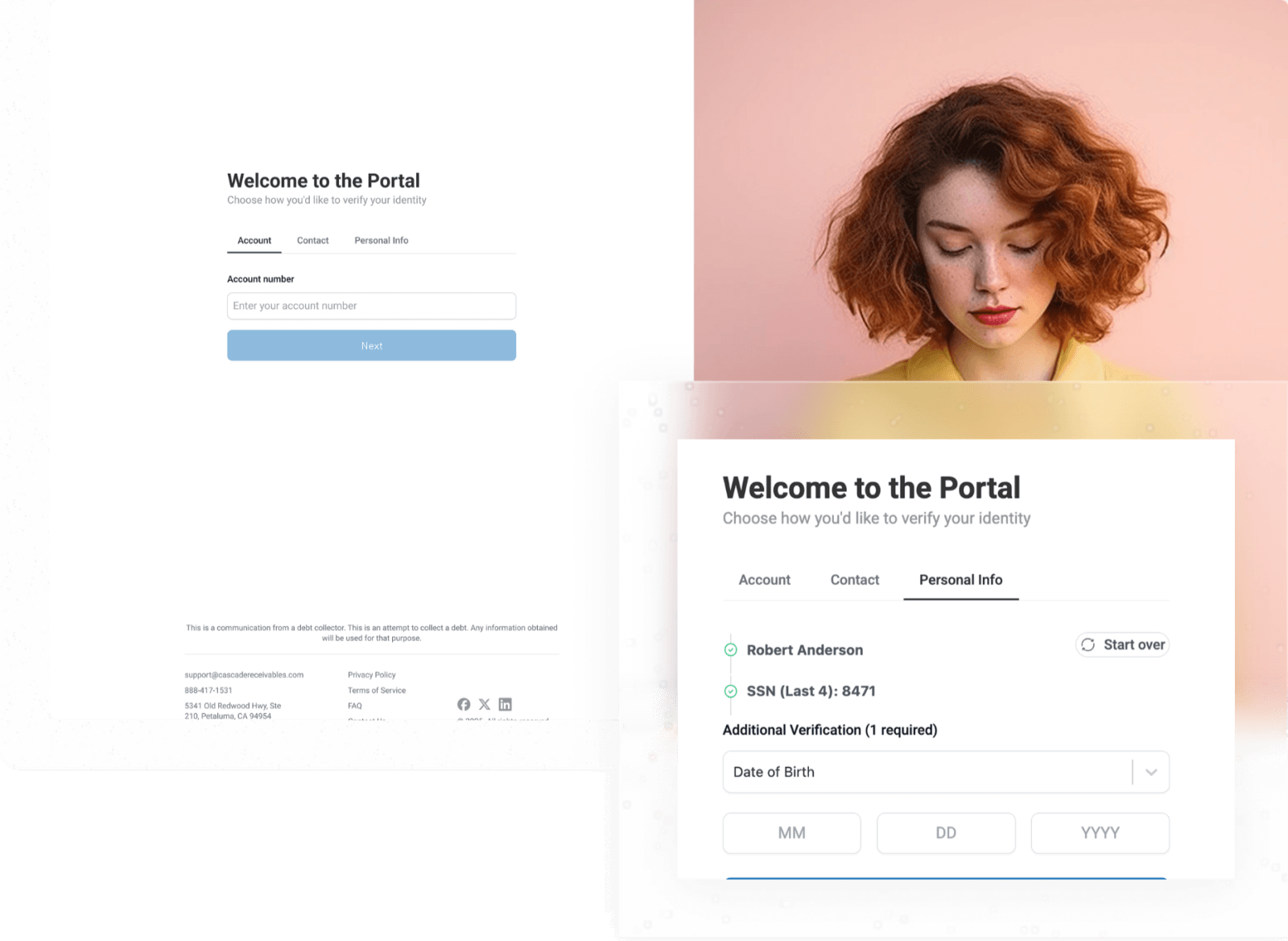

What a portal built to convert actually looks like

Don't take our word for it. Look at it.

What's different:

- One-step verification via a secure, time-bound link — no account numbers to remember

- Mobile-first design that works the way consumers expect

- Your branding throughout — building trust from the first click

- Payment plans front and center — a path, not just a number

- Multiple accounts in one place — consolidated into a single, manageable plan

This is the experience consumers are already used to everywhere else. Your portal is being measured against it, whether you like it or not.

But a better-looking portal is just a promise. What matters is whether it collects. Here's what happened when one firm closed the gap.

One law firm went from 34% to 92% verification completion rate

Same portfolio. Same consumers. Same outreach spend. The only thing that changed was the portal — text-to-portal delivery with pre-filled account data, one-step verification, and AI-recommended payment offers.

The results:

- Verification completion jumped from ~34% to 92% — the same consumers who were bouncing at the front door were now getting in

- Time to complete a payment dropped to under 2 minutes — and under 60 seconds for returning consumers with a saved payment method

- 66% chose the AI-recommended offer — they didn't need to negotiate, they needed a reasonable path

The outreach spend didn't change. The portal did. That's where the money was hiding — in the gap between what your text message promised and what your portal delivered.

See how law firms are winning more placements by improving collections performance →

Forward this to whoever manages your portal — with these 6 questions

Ask them today:

- What is our verification completion rate right now?

- What percentage of consumers who land on our portal leave without paying?

- How does our portal look on a mobile phone?

- Does our portal pre-fill account information from the links we send?

- What did we pay for this portal in the last 12 months — and what has it collected?

If the answer to most of these is "I don't know" or "we haven't" — you now know exactly where to start.

Your consumers are showing up. Make sure your portal is ready to receive them.